__PRESENT__PRESENT

__PRESENT__PRESENT__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT__PRESENT__PRESENT__PRESENT__PRESENT

Author: Rob Crookston, Lead Strategist, Bell Financial Group

The recent escalation in the Middle East has generated sharp, broad-based market volatility. The moves have been swift but based on a long historical record, they are also most likely temporary.

What Markets Have Done

The initial moves across asset classes have been consistent with prior episodes of geopolitical stress:

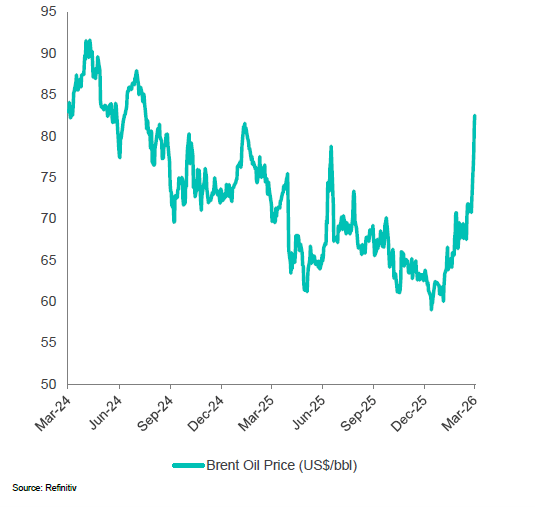

- Oil and gas prices surged as markets moved to price in potential supply disruption from a key producing region.

- European gas prices rose sharply, reflecting the continent’s particular sensitivity to energy supply security.

- Global equities fell, with the steepest declines in sectors most exposed to energy costs and travel demand, including airlines and logistics.

- Shipping through the Strait of Hormuz, through which ~20% of global oil and gas flows, has effectively stopped following the strikes.

- Concerns have also emerged around potential damage to regional energy infrastructure, which could tighten energy markets further if sustained.

- These moves reflect a rational response to a sudden increase in uncertainty, with markets pricing in an uncertainty premium.

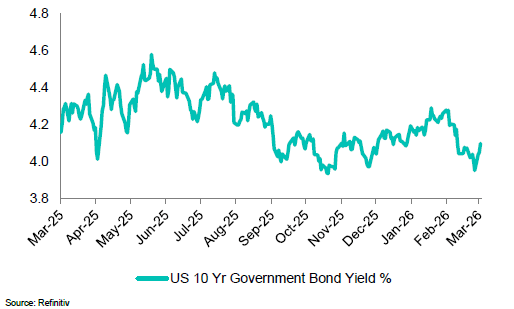

Bond markets have sold off indicating fear over inflation rather than fear over growth. The oil price would have to be significantly higher for growth concerns to emerge:

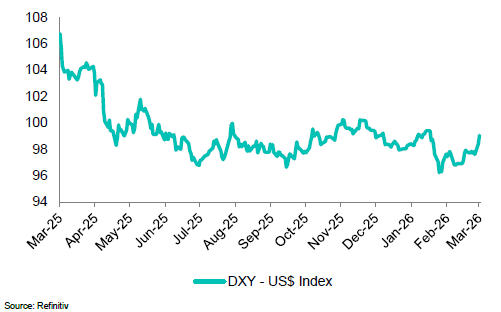

The Iran conflict reinstated the US dollar safe haven appeal:

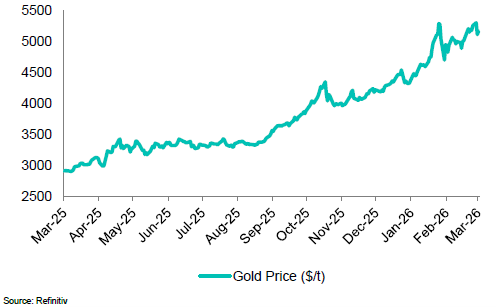

Gold has fallen because the conflict driven spike in oil prices sparked fears of “higher-for-longer” interest rates and a surging US dollar, prompting investors to liquidate the non-yielding metal for cash and meeting margin calls:

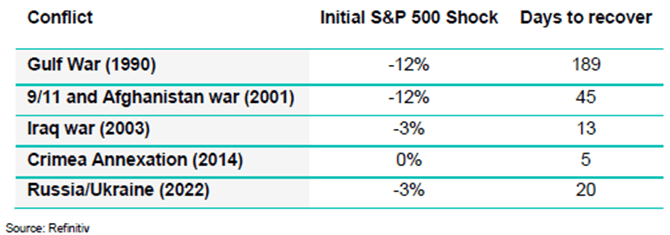

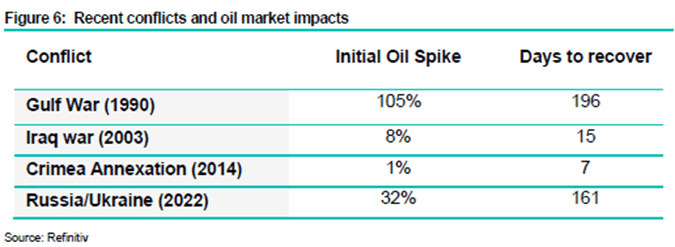

What History Tells Us

The historical record on geopolitical shocks and financial markets is consistent. Conflicts produce fear, volatility, and near-term dislocations. They rarely produce the kind of sustained, structural damage that permanently impairs long-term investment outcomes.

This pattern has held across the September 11 attacks (coinciding with the invasion of Afghanistan), the Iraq war, Crimea annexation and Russia’s invasion of Ukraine in 2022. Each produced an initial risk-off phase marked by equity weakness and safe haven demand. In each case where the conflict remained contained and did not coincide with a broader financial crisis, equity markets recovered.

From an investment strategy perspective, the challenge lies in the velocity of the market’s response to geopolitical news. While a perfectly timed exit and entry would be the ideal outcome, these episodes are often defined by rapid V-shaped recoveries. Sentiment can shift on a single headline; therefore the risk is that investors miss the sharpest leg of the rebound, which has historically proven more damaging to long term performance than weathering the initial volatility.

Risks Worth Monitoring

This is not to minimise the genuine risks present in the current situation. The Strait of Hormuz is a real vulnerability, with ~20% of global oil transit going via the Strait. A sustained disruption to transit through this chokepoint would represent a significant global energy supply shock, with consequences for inflation, growth, and central bank policy that would extend well beyond the region. Elevated oil prices, even without that scenario, add to near-term inflation, reduce room for central banks to ease, and weigh on global growth, all negatives for equity markets.

The conditions that would require a more cautious reassessment are:

- The conflict broadens to involve additional state actors, extending the geographic scope of risk.

- Damage to regional energy infrastructure proves sustained rather than short-lived.

- Oil prices move to levels historically associated with demand destruction and recession (beyond the current ~US$80/bbl price). The encouraging news for inflation was that the global oil market was in a healthy surplus at the start of 2026.

- OPEC is unable or unwilling to deploy spare capacity to offset supply disruptions.

These are still risks rather than our base case; however, they carry real consequence and warrant monitoring.

The Bottom Line

Risks are rising and should be monitored but a start of a conflict is not typically a catalyst for a prolonged sell-off. The historical precedent across a wide range of geopolitical episodes is clear: well-diversified portfolios, held with discipline through periods of uncertainty, consistently produce better outcomes than those managed reactively. There is no strong case for imminent repositioning.