__PRESENT__PRESENT

__PRESENT__PRESENT__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT__PRESENT__PRESENT__PRESENT__PRESENT

Weekly Wrap Transcript 1 March

We are in the final few weeks of reporting season and so far, 346 companies have reported. 114 of these have beat expectations, 135 have met expectations and 97 have missed expectations. While investors have been very reactive to results, both sending share prices soaring and plummeting, brokers have been more reactive to downgrades than upgrade ratings with 40 upgrades and 47 downgrades from brokers so far.

Let’s dive into the final reporting season coverage video, and discuss the overall themes identified over the first half that will pave the way for 2H24.

Anticipation of a rebound in the Australian home building sector over the coming years boosted outlook and investor sentiment for white goods retailer Harvey Norman (ASX:HVN) later this week after the company reported a slow down in first half activity. For the first half, Harvey Norman reported a 6.8% decline in total system sales revenue, a 23% decline in the interim dividend to 10cps and profit before tax declined for the fourth consecutive time in the first half since H1 2021, by 45.7% on the PCP, however, is still above pandemic levels. The results were unsurprising in this easing consumer spend environment. Harvey Norman’s value also comes from its property portfolio which stood at $4.14bn in 1H24 which is a very strong support for the company’s balance sheet. Investors shrugged off the weaker first half results sending HVN shares up over 4% on Thursday after the results were released.

For the retailers this reporting season, Lovisa (ASX:LOV), and JB Hi-Fi (ASX:JBH) have stood out as clear winners with resilience and growth outlook amid the easing consumer spend environment. Given retail spend in January rose just 1.1% which fell short of expectations for 1.5% growth, retailers will need to brace for eased spend for a little time to come.

Over in the healthcare department, investors were quick to snap up shares in Ramsay Healthcare (ASX:RHC) after the company released first half results, but this was a surprising reaction given the company’s performance in the first half. For the period, Ramsay reported a 13.8% rise in revenue to $8.1bn, EBIT declined 4.7%, NPAT dropped 23% to $140.4m and a fully franked DPS was declared of 40cps. Ramsay attributed the weaker results to weakness in the AUD against EUR and GBP, and lower earnings from the European region. While the first half results were weaker, investor confidence in the leading global hospital group may be driven by the outlook in the company’s report including the implementation of cost cutting measures and the expectation for profit growth for the full year despite a decline in H1.

Across the healthcare companies this reporting season, ResMed (ASX:RMD) was the standout for beating expectations across the board and reporting a long-awaited improvement in gross margins, and squashing any concerns of a risk that demand could decrease due to the recent introduction of weight loss drugs like Ozempic. ResMed’s closest competitor for sleep apnoea devices in the US, Philips, is also still delayed in its attempts to return to the US market following a previous recall of its devices, so this is likely to remain a strong performing market for ResMed into the future.

The miners have made little impact on share and sector performances this reporting season naturally as their respective performance and results are driven by changes in commodity prices and demand which for the first half of FY24 was turbulent across the board, especially for iron ore and lithium producers. BHP (ASX:BHP) and Rio Tinto (ASX:RIO) met expectations for the first half despite weaker demand out of China, Mineral Resources (ASX:MIN) beat expectations with higher-than-expected revenues from its mining services division, and Piedmont Lithium (ASX:PLL) missed expectations for Q4 in reporting a net loss of $25.4m and a decline in revenue amid the sliding price of lithium.

Overall reporting season for February 2024 has been a relatively evenly mixed bag between beats and misses and sets the foundations for an interesting second half with the expectation of the following themes to continue into 2H24:

- China’s recovery will continue to impact the miners and any company with exposure to the region.

- Retailers will continue to face eased consumer spend, but this may bode well for some niche retailers.

- Full year dividends will be the key to winning investors back come August reporting season.

- Cost management has been a downfall in H1, will companies rectify this in H2?

- Margin expansion should be a key focus heading into the second half of FY24.

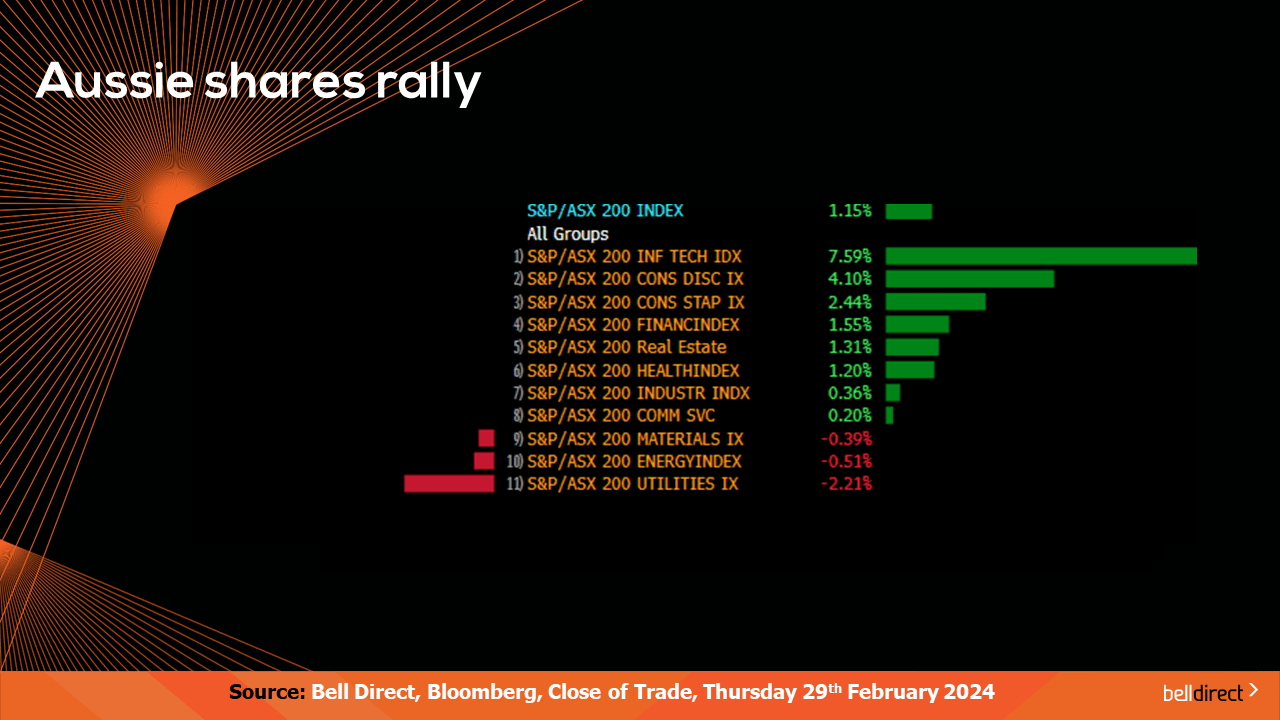

Locally from Monday to Thursday the ASX200 rose 1.15% on favourable economic data including Australia’s inflation rate remaining steady over the last month, and on the back of some strong corporate results being released. Information technology stocks did most of the heavy lifting with the sector rallying 7.6% over the four trading days, while utilities and energy stocks weighed on the key index this week.

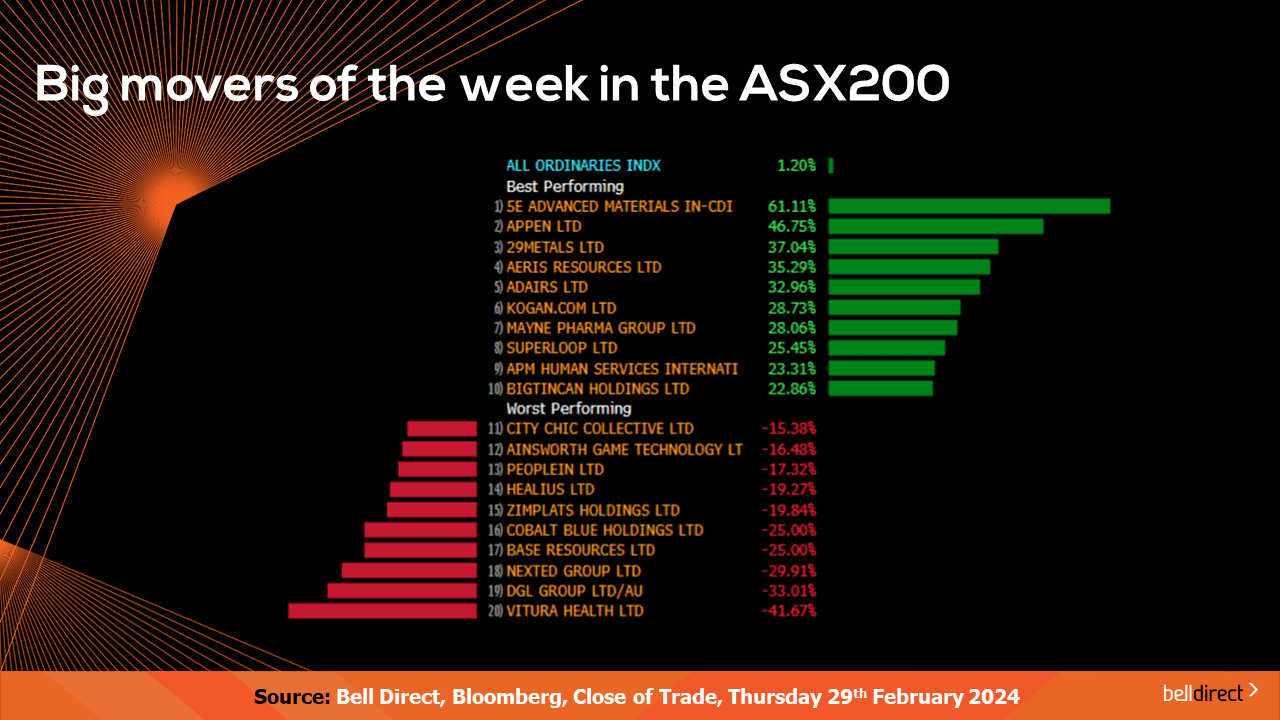

The winning stocks from Monday to Thursday were led by Block Inc. (ASX:SQ2) soaring 19.18% on strong first half results, Lovisa (ASX:LOV) jumping 18.83% for the same reason, and NextDC (ASX:NXT) also adding 18.54% again, for the release of very impressive H1 results.

On the losing end, Healius (ASX:HLS) tanked nearly 20% while Sayona Mining (ASX:SYA) fell 13% this week.

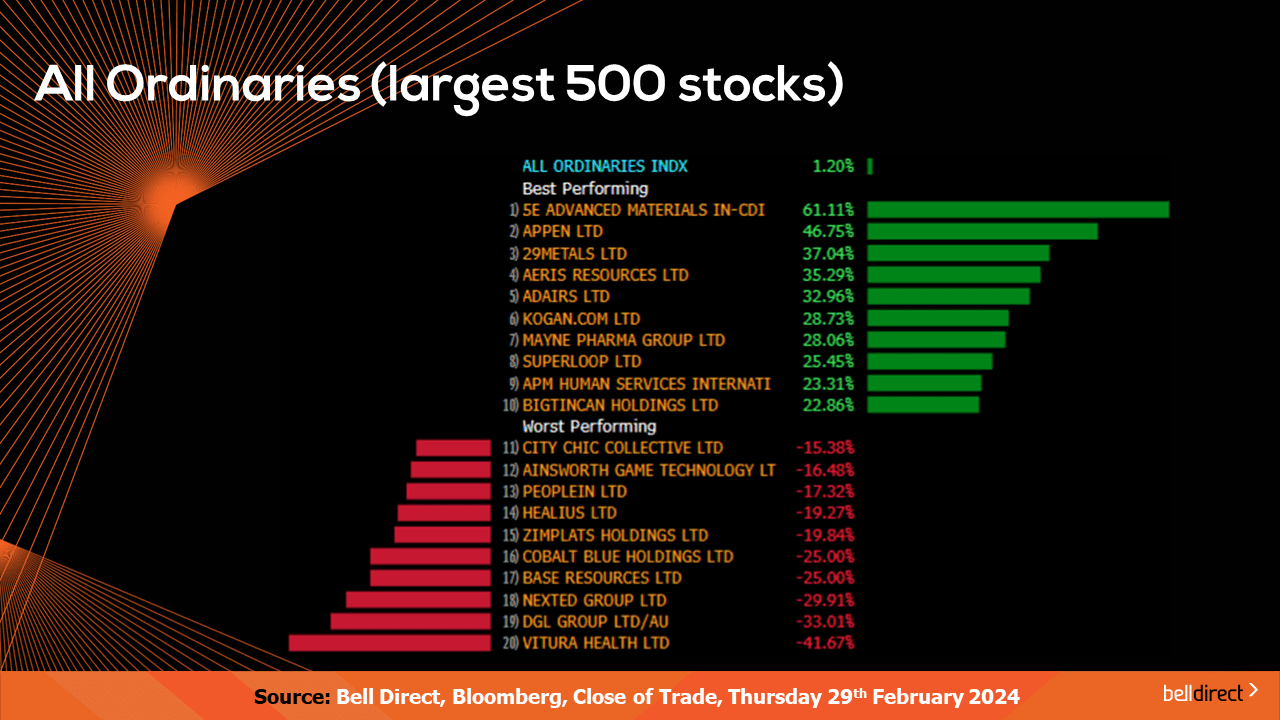

Looking at the broader market, the All Ords rose 1.2% this week as 5E Advanced Medical (ASX:5EA) rocketed 61% on release of an operational update, while Appen (ASX:APX) added almost 47% this week.

Vitura Health (ASX:VIT) and DGL Group (ASX:DGL) weighed on the All Ords this week, falling 42% and 33% respectively.

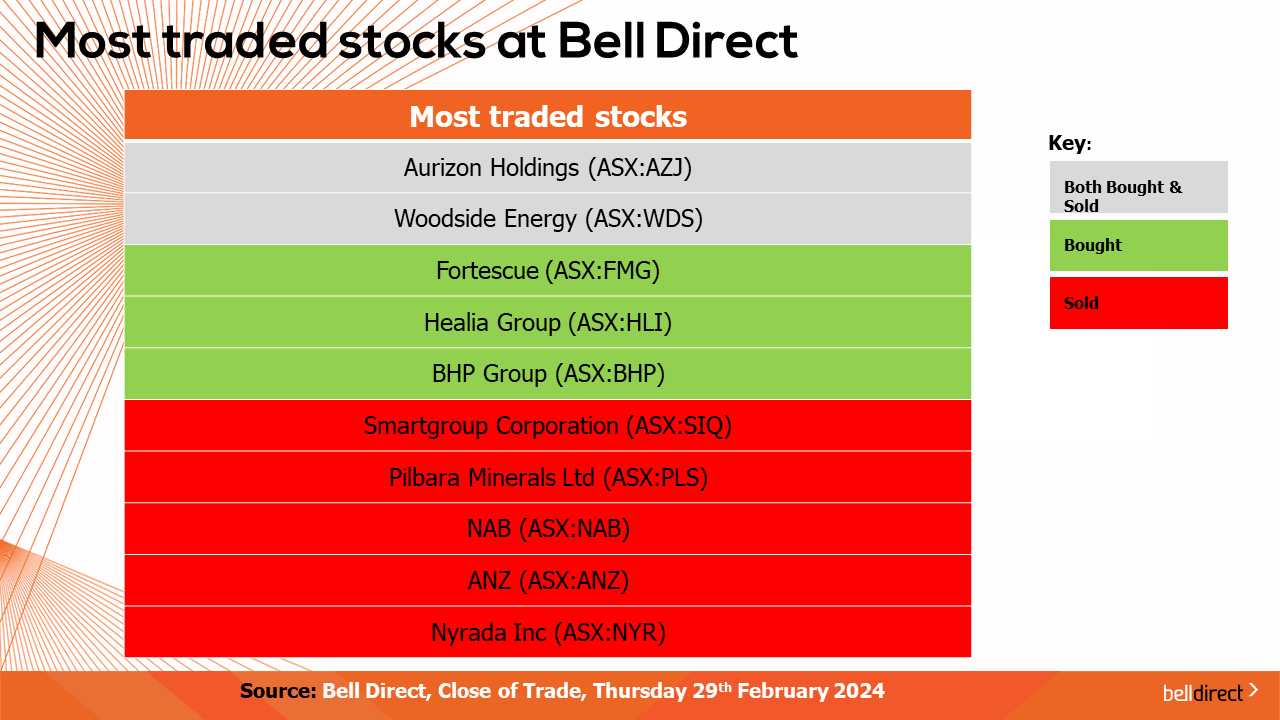

The most traded stocks by Bell Direct Clients over the four trading days were Aurizon Holdings (ASX:AZJ) and Woodside (ASX:WDS). Clients also bought into Fortescue (ASX:FMG), Healia Group (ASX:HLS), and BHP Group (ASX:BHP) while taking profits from Smartgroup Corporation (ASX:SIQ), Pilbara Minerals (ASX:PLS), NAB (ASX:NAB), ANZ (ASX:ANZ) and Nyrada (ASX:NYR) Inc.

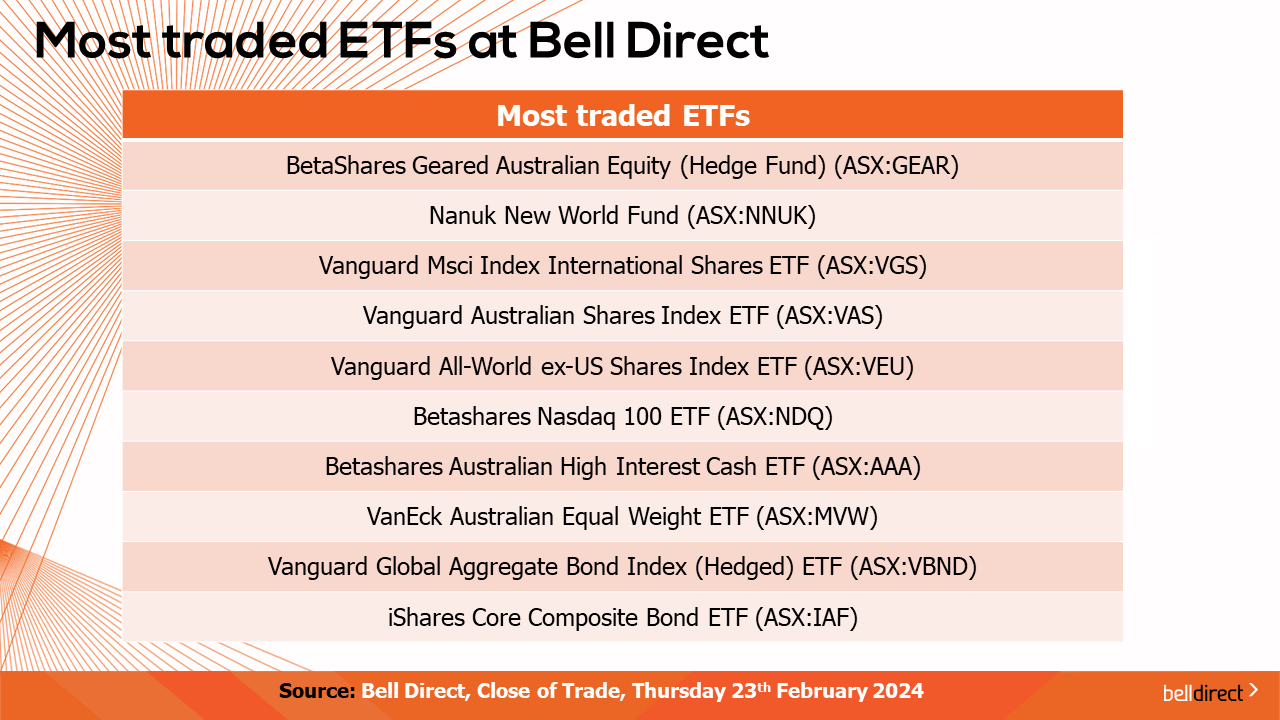

The most traded ETFs by Bell Direct clients this week were led by BetaShares Geared Australian Equity (Hedge Fund), Nanuk New World Fund (Managed Fund), and Vanguard Msci Index International Shares ETF.

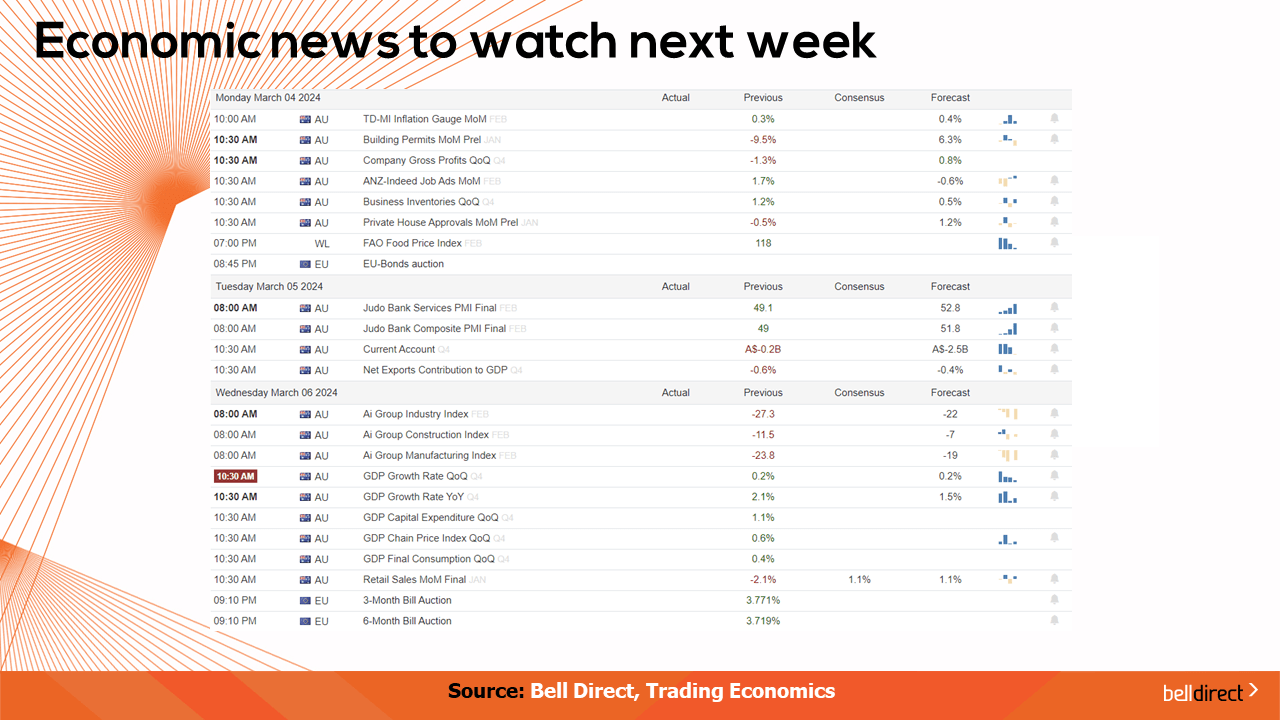

Looking ahead to next week on the global economic calendar, Australia’s all-important GDP growth rate data for Q4 is released on Wednesday with the expectation of 0.2% growth which is inline with the previous quarter’s growth rate. The nation’s trade balance is also out on Thursday for January which will indicate whether Australia’s trade surplus continued to decline or rebounded in January.

Overseas, key US jobs data will likely impact Wall Street sentiment over the week with JOLTs Job Openings data, Non-farm payrolls and unemployment rate data all out later next week.

And that’s all we have time for today, have a wonderful weekend and happy investing!