__PRESENT__PRESENT

__PRESENT__PRESENT__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT

__PRESENT__PRESENT__PRESENT__PRESENT__PRESENT

Transcript: Weekly Wrap 27 October

Thank you for joining me this Friday the 27th October, I’m Grady Wulff, a Market Analyst with Bell Direct and this is the weekly market update.

Higher fuel prices, rising rental costs and increased electricity prices were the key drivers of Australia’s inflation rate rising 1.2% in the September quarter, which is unsurprising as these drivers have remained the sticky points in taming inflation. The reading rising however, works against the RBA’s efforts to tame inflation to the target 2-3% range. Economists’ were expecting an annual rate of 5.3%, down from the 6% reading reported in Q2, however the data came in at 5.4% which is slightly higher than was expected.

According to Bloomberg, investors have factored in an 80% chance of a 25-basis point rate hike at the next RBA meeting on November 7, up more than double in just a day after the latest CPI data was released. Additionally, all four big banks now expect the RBA to hike the nation’s cash rate to 4.35% on Melbourne Cup Day, whereby before the CPI results were released, only NAB was expecting another rate hike.

At a Senate estimates hearing on Tuesday, new RBA Governor, Michele Bullock told the hearing she expects annual rental prices will increase to 10% in the coming months ‘before moderating’. So what will a 25-basis points rate hike look like for your portfolio, the cost-of-living crisis and Aussie businesses?

If you own a property with the average home loan in Australia of $500,000, you can expect to pay an extra $83.30 per month on your repayments, bringing the total to $3303/month. That’s up almost 50% from April 2022.

The cost-of-living crisis will only worsen if the RBA hikes the cash rate to 4.35% at the November meeting. Australians are battling higher fuel costs, rental price rises and the cost of everyday services are increasing. The only respite has come from everyday goods which are likely to remain subdued as goods inflation eased to a near two-year low in Q3.

What this means for businesses and more specifically your portfolio is:

- Assess each company you are invested in to determine their level of debt – remember debt repayments increase with every interest rate hike.

- Analyse whether the company has had to absorb or has successfully passed on rising costs to customers over every rate hike to date.

- Consumer discretionary spend is likely to slide further as the basic cost of living continues to bite.

We are not suggesting a rate hike is guaranteed come Melbourne Cup Day, however, with all four big banks now expecting the RBA to announce another 25-basis point hike on November 7, it’s best to prepare for the unfavourable scenario.

Quarterly trading updates and results continued being released this week and as usual, investors reacted with some strong market moves in response.

Lithium giant Pilbara Minerals (ASX:PLS) fell out of favour with investors on Thursday after releasing a first quarter update outlining production down 11%, sales down 17% and costs up 16% in the first quarter.

Megaport (ASX:MP1) followed suite, tanking almost 20% on Thursday, after releasing its latest quarterly update. The sell-off may have been overdone as part of the widespread tech sale on Thursday following the Nasdaq’s worst session in 2023 on Wednesday. Megaport may have reported record earnings and positive cash flow, but investors seemed more concerned about the company being in ‘rebuild and recovery’ mode according to chief executive Michael Reid, after customers grew 0% on the prior quarter and revenue rose just 5%.

With sell-offs there are certainly opportunities to buy in the market, so do your research and analyse both the company’s own outlook alongside the economic outlook before making any investment decisions.

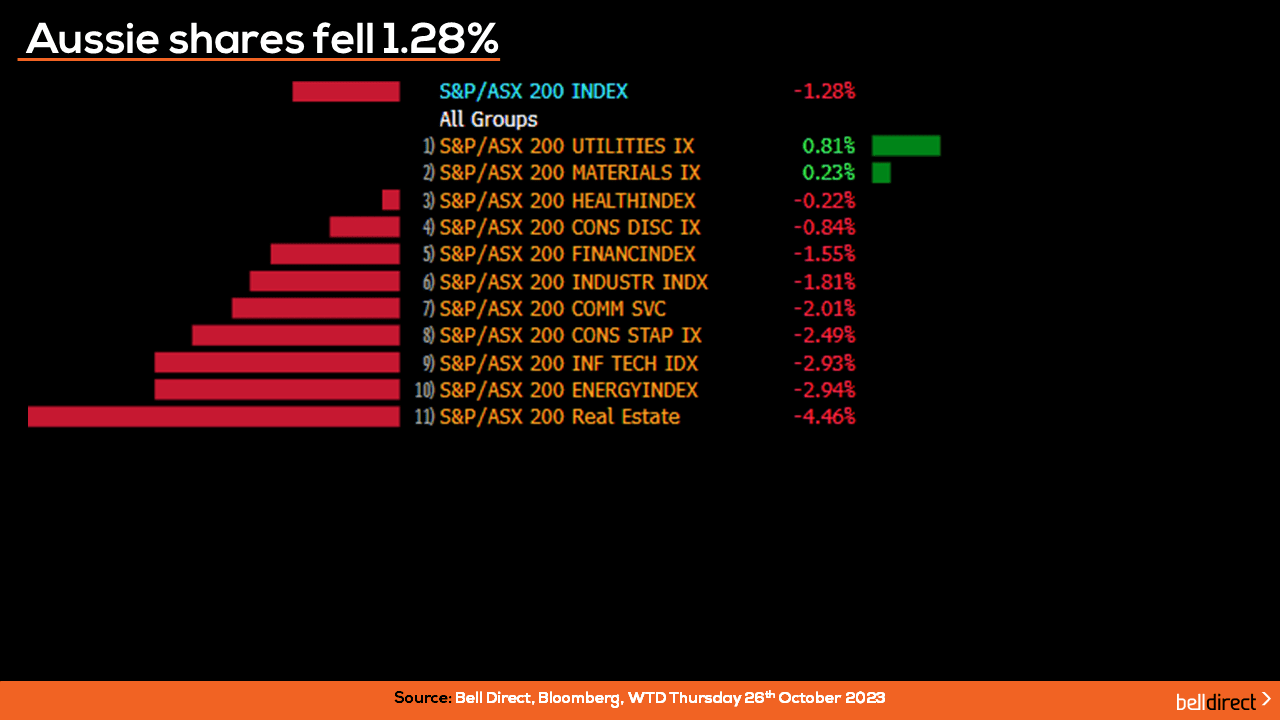

Locally from Monday to Thursday, the ASX200 fell 1.28%, weighed down by the REIT sector falling almost 4%, while energy stocks fell just shy of 3% on the retreating price of oil. Utilities stocks were the only sector to close in the green over the four trading days.

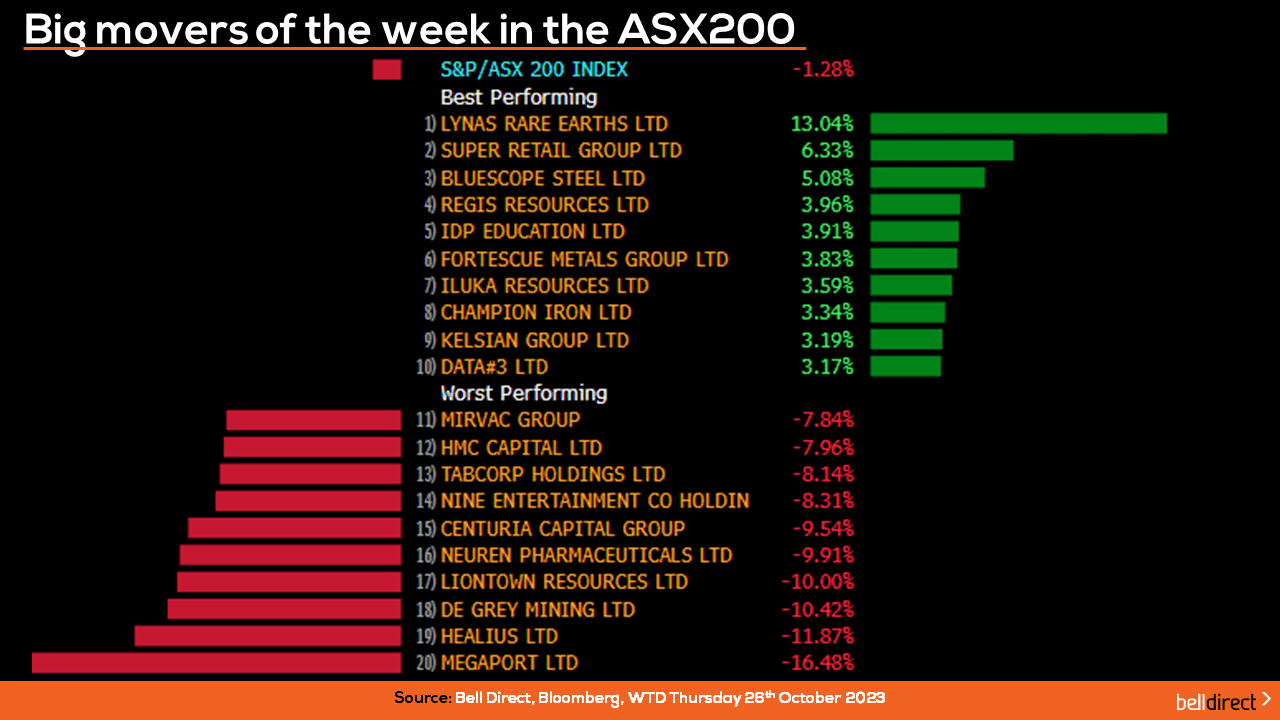

On a stock specific note, Lynas Rare Earths (ASX:LYC) topped the ASX200 this week, gaining over 13% after the rare earths producer provided an update on its Malaysian licence including an extension of importation of lanthanide to its Malaysian facilities from the Kalgoorlie operations. Super

Retail Group (ASX:SUL) rose 6.33% over the week, and Bluescope Steel (ASX:BSL) rallied 5.08%.

Megaport weighed down the ASX200 this week, falling 16.5% on the release of that first quarter trading update, while Healius (ASX:HLS) and De Grey Mining (ASX:DEG) lost 11.9% and 10.42% respectively.

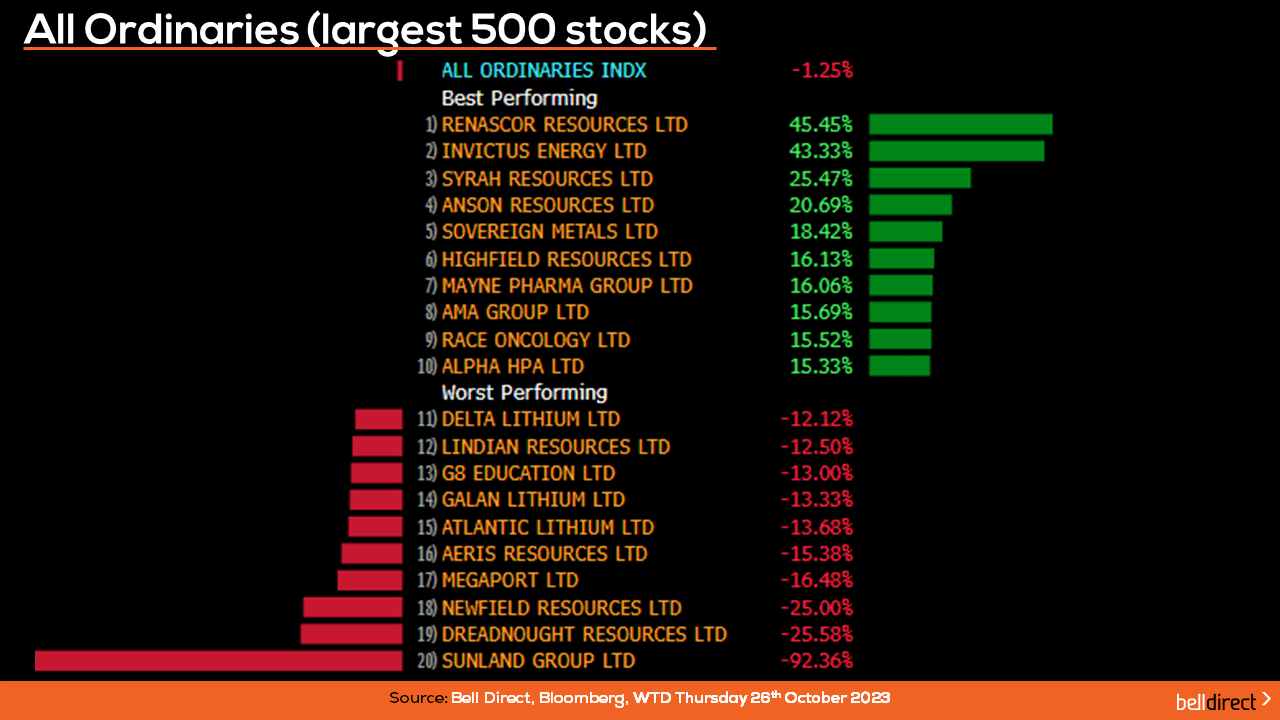

The All Ords fell 1.25% this week as Renascor Resources (ASX:RNU) soared 45.45% to offset some of the losses among the broader index. Sunland Group (ASX:SDG) tanked 92.36% over the four trading days though as the company’s shares traded ex-capital return, meaning the rights to an upcoming return are now settled in and new buyers of Sunland shares will not be entitled to it.

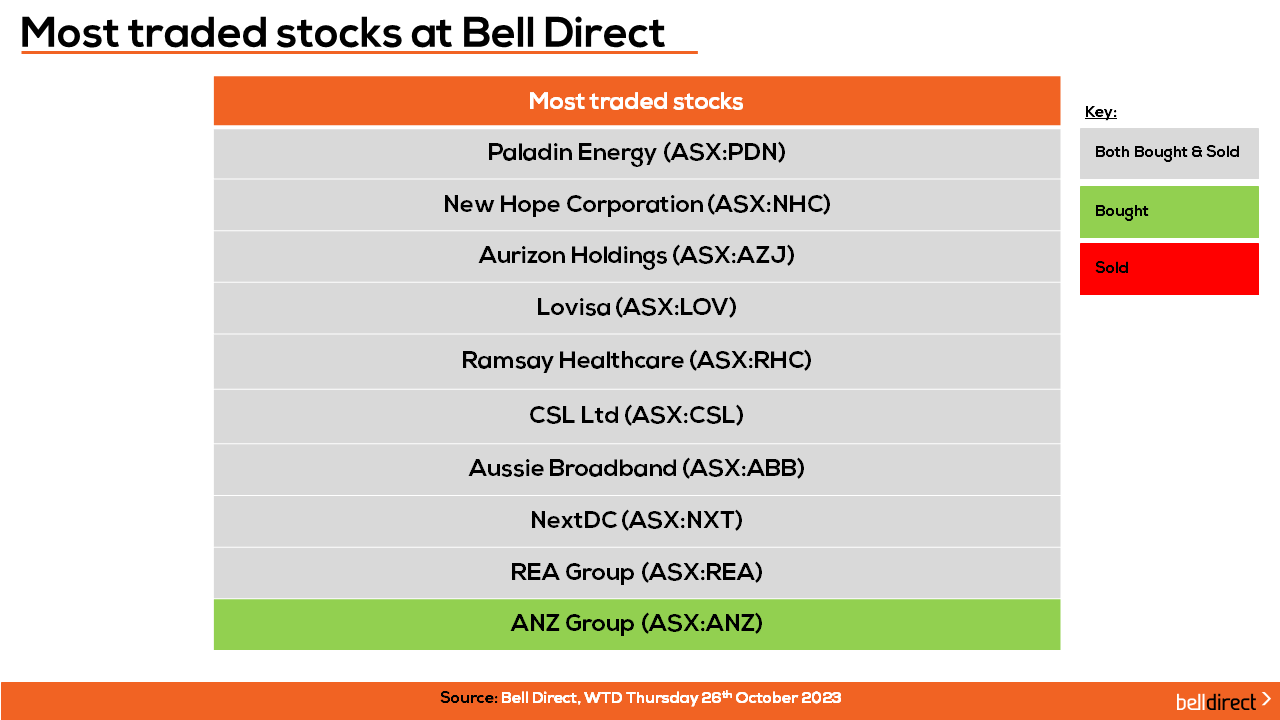

The most traded stocks by Bell Direct clients over the four trading days were, Paladin Energy (ASX:PDN), New Hope Corporation (ASX:NHC), Aurizon Holdings (ASX:AZJ), Lovisa (ASX:LOV), Ramsay Healthcare (ASX:RHC), CSL (ASX:CSL), Aussie Broadband (ASX:ABB), NextDC (ASX:NXT) and REA Group (ASX:REA).

Clients also bought into ANZ (ASX:ANZ) this trading week.

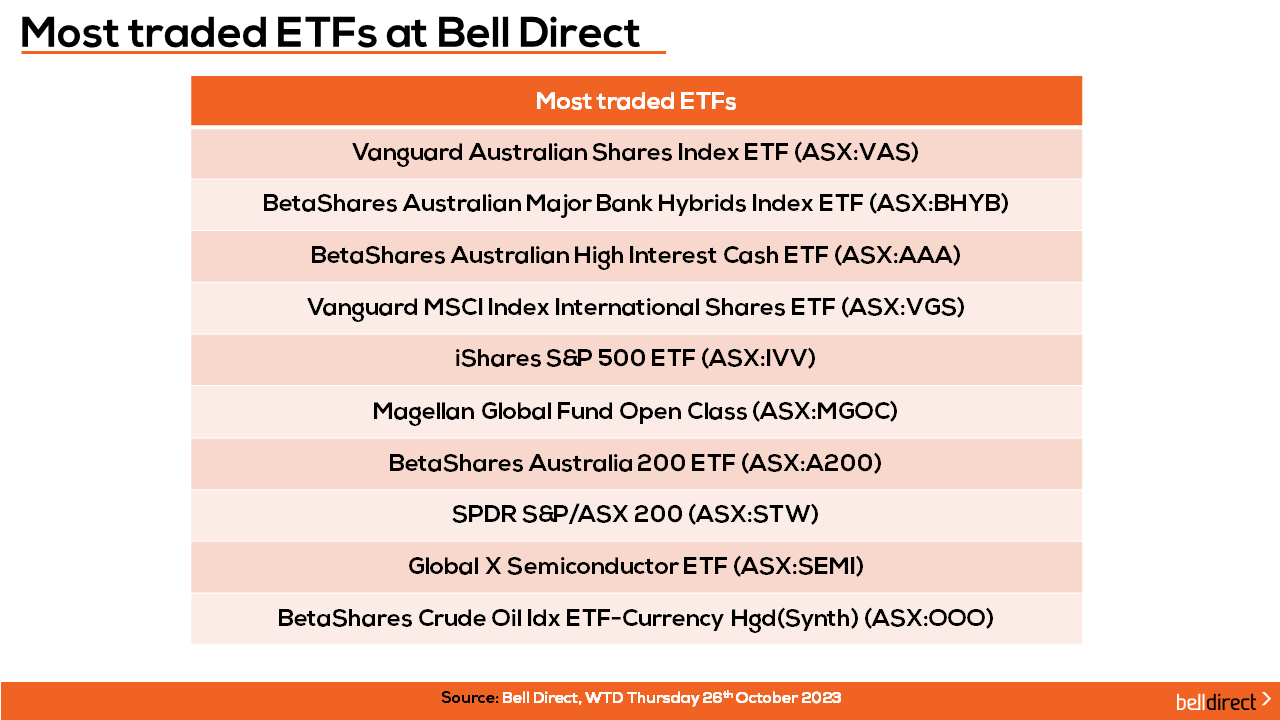

And the most traded ETFs were led by Vanguard Australian Shares Index ETF, BetaShares Australian Major Bank Hybrids Index ETF and BetaShares Australian High Interest Cash ETF.

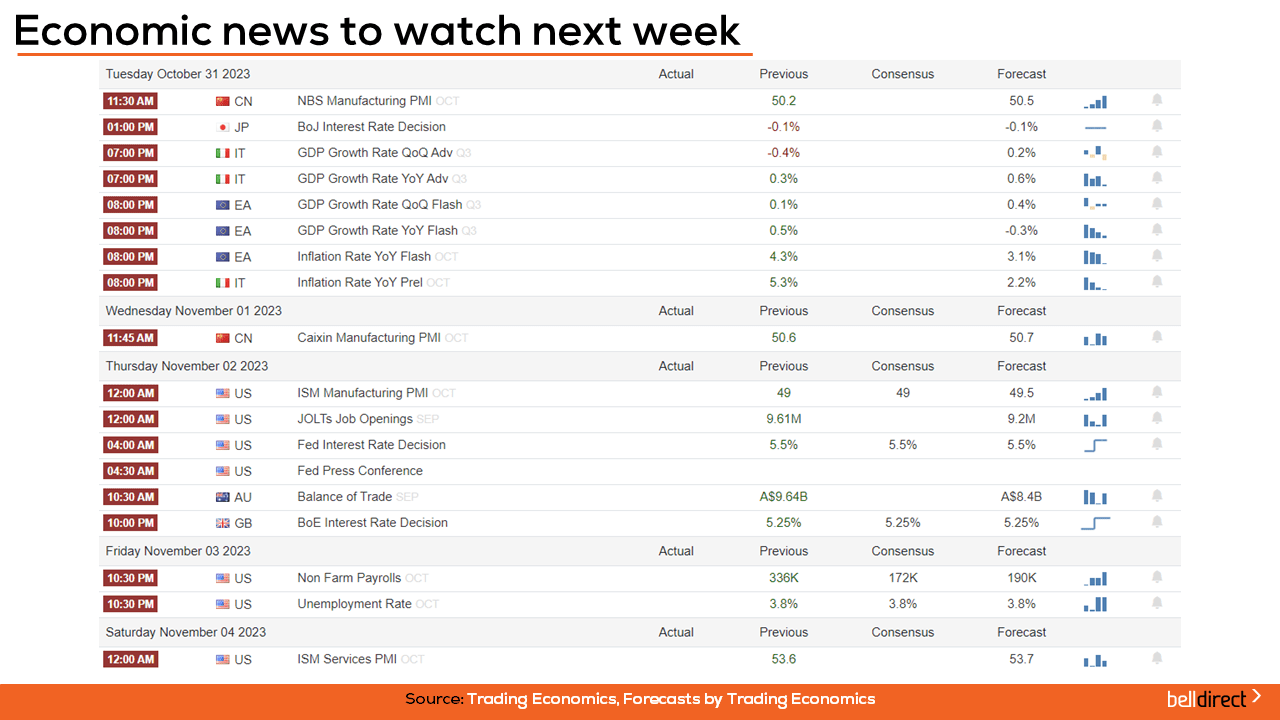

Looking at the week ahead, it’s a big week on the European calendar with Italy, Germany and the European region’s respective GDP growth rate readings out early in the week, while over in Japan, the Bank of Japan will hand down the latest interest rate decision on Tuesday with the market expecting the announcement of the -0.1% rate to be maintained for yet another month.

Locally, Australia’s balance of trade data is out later in the week with the expectation of a further decline in the country’s trade surplus to $8.4bn from $9.64bn in August, and over in the US, it’s a big week on the jobs front and the Fed will hand down the latest rate decision with the expectation of a hold.

So, a lot of exciting developments in markets this week, and much to watch out for next week. Have a wonderful weekend and as always, happy investing!